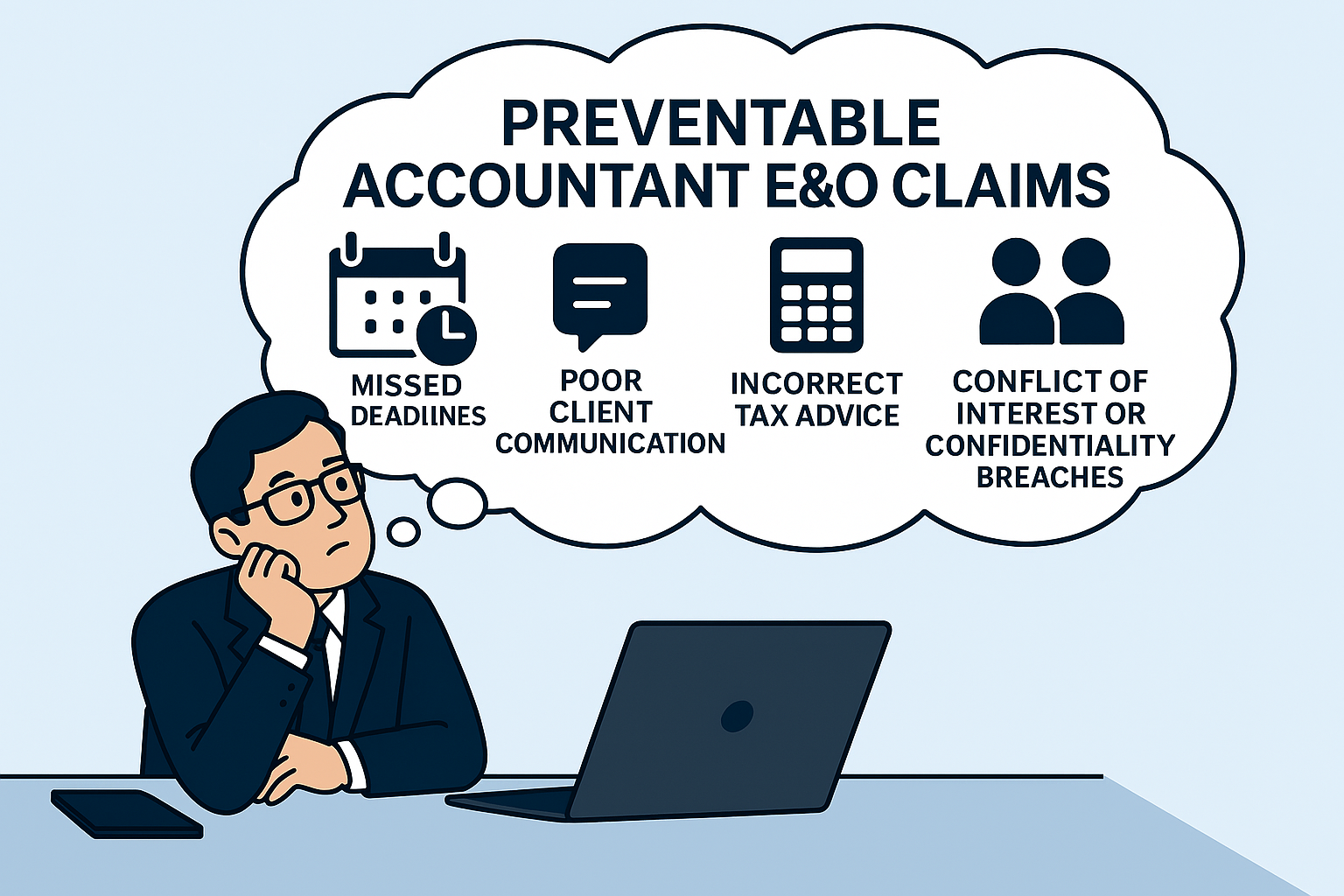

Top 5 Preventable Causes of Accounting E&O Insurance Claims

- Missed Deadlines (e.g., tax filings or audits)

Cause: Overlooked due dates or mismanaged calendars.

Prevention: Implement dual docket controls and automated reminders. Cross-check deadlines with clients and confirm receipt of all necessary documents. - Failure to Communicate Clearly

Cause: Misunderstandings about scope, deliverables, or changes in tax law.

Prevention: Use engagement letters that clearly define services. Document all client communications and confirm major decisions in writing. - Incorrect Tax Advice or Misinterpretation of Regulations

Cause: Misapplying tax codes or overlooking recent changes.

Prevention: Stay current with continuing education and subscribe to trusted tax law updates. When in doubt, consult a specialist or legal counsel. - Data Entry or Calculation Errors

Cause: Manual mistakes in financial statements or returns.

Prevention: Use reliable accounting software with built-in checks. Have a second set of eyes review critical outputs—especially for high-stakes filings. - Conflict of Interest or Breach of Confidentiality

Cause: Representing clients with competing interests or mishandling sensitive data.

Prevention: Maintain a robust conflicts-check system and enforce strict data security protocols. Regularly train staff on confidentiality and ethics.

Accounting Errors & Omissions Claims isn’t just about making a mistake, it’s about systems, habits, and culture. A strong errors & omissions insurance policy (APL) is critical, but risk prevention begins with the daily choices inside the firm.

Contact Me Today

Lee Norcross, MBA, CPCU

California License # 0D87292

L Squared Insurance Agency, LLC ® DBA in California as L2 L Squared Insurance Agency, License # 0L93416

Managing Director, CEO

Lee@L2Ins.com

616-726-7080

![]()